Fort McMurray, earthquakes, ice storms and floods—we have all seen the headlines about natural disasters and how they affect individuals, businesses, and whole communities.

Fort McMurray, earthquakes, ice storms and floods—we have all seen the headlines about natural disasters and how they affect individuals, businesses, and whole communities. When you are involved in running a captive insurance company, these issues are not just something you read about in the paper, they affect your company, your operations, and your personal credibility as a manager or executive of that operation. The big questions are always: how ready are you, and how do you know you are ready?

But we complied with all the rules

In many captives, risk management has become a generic concept. It focuses on compliance with the rules—whether the captive has enough cash on hand, completed the requisite forms and filings, and followed company protocol. But when a financial disaster hits your captive, it will be little comfort to the board if you tell them that even though they are now insolvent, it is not your fault. After all, you complied with all the rules, what more did they want? The answer is quite a bit, actually. Boards expect management to be prepared and proactive, not merely compliant.

So it is not surprising to find boards asking, just how safe are those government rules? Does the regulatory capital limit protect us from a 1-in-10-year event or from a 1-in-100-year event? The regulatory rules do not answer that question for you. It may very well be that the government rules are more than adequate, but you may want some sort of analysis to support that statement, rather than just take it as a given.

To do this, you need your own assessment of how much risk you are exposed to, how likely you are to draw on your capital, and whether your capital is sufficient. You would also need to determine and justify at what point can you sleep well at night knowing that you are prepared.

Risk management does not mean risk avoidance

Some companies we work with respond to the concern of adverse claims by passing off even more of their risk to reinsurance companies. A good reinsurance programme will certainly reduce your downside risk, but it comes at a cost in the form of reinsurance premiums that are paid even when times are good. What is the right trade-off?

The same risk assessment models that help you decide whether your capital is adequate can and should be used as tools to help you strike an optimal balance of risk and reward in your reinsurance strategy. If you had access to more capital, you could retain more risk and spend less on reinsurance. Conversely, with more reinsurance, you could release some of your capital to your owners or stakeholders.

In determining the optimal reinsurance strategy, the board needs to consider whether it could withstand some year-to-year fluctuations if that produced a lower overall cost, or do they want stable results every year? Adding further sophistication, is there some way to diversify the risks, rather than just think in terms of the one-dimensional more/less view?

Complex math, understandable explanations

We, as actuaries, have a tendency to come up with rather complex math as a way to analyse and quantify risk. While some statisticians might disagree, our charts are some of the best in the business.

However, the analysis and charts are just tools, the objective of all this complex math is to help management do a more effective job of managing their business.

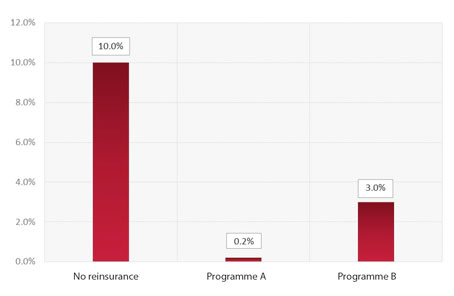

For example, you are running a captive and worried about the downside of adverse claims, and trying to decide between reinsurance programme A and reinsurance programme B. As a baseline, you also look at results without any reinsurance, what are the odds of losing money overall under none, A and B options? The answer to in this Chart 1.

Chart 1: Probability of losing money

The no reinsurance option looks like it will result in a loss once every 10 years, which is probably not acceptable, but now you have quantified your exposure in a meaningful way rather than just saying it would be “too risky”.

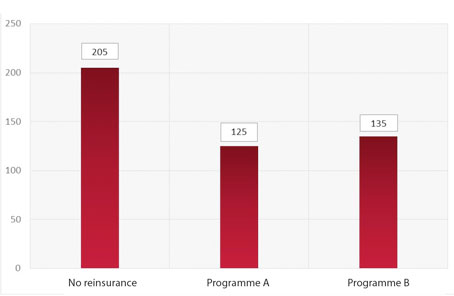

Programme A looks like the clear winner, with a loss less than once in every 100 years, but at what cost? Chart 2 shows the average profit of the three options.

Chart 2: Average profit

Programme A costs $80 per year, but the question is whether that is an acceptable cost given the fifty-fold reduction in the odds of losing money. Programme B does not look nearly as enticing given that it costs $70, however has a much higher chance of losing money.

Neither of these charts answer the question of how much reinsurance is the right amount, but the point is that you have numbers to work with and base your decision on. If the losses under programme B are considered manageable, given its lower cost, it might still be a better fit.

Maybe you can live with the downside?

The right risk analysis can lead to some surprising insights and show that sometimes concerns are overstated. Yes, there is an exposure, but it may not be as likely or not as severe as you think.

The right analysis can put some numbers on it. In one case we worked on, the ‘worst case’ that everyone was worried about translated into a 25 percent increase in fees for their members.

A 25 percent increase is presumably something that management would like to avoid, but hardly the end of the world as worst cases go. With that analysis in hand, the company was able to move forward with more confidence than it had previously.

Your actuary can be your friend

Everyone agrees there is risk out there and it needs to be managed, however there is a smart way to do it beyond just following the rules or avoiding risks.

With help from your friendly neighbourhood actuary, risk can be your friend if you are prepared for it. The right risk analysis can help you navigate the way forward.